Policy & Insight Team, 14th May 2025

Each month, the Policy and Insight team review datasets which give us an idea of how our local economy is doing. This helps us identify key challenges and respond to them. We put this information in an overview report which you can find on our Intelligence page.

This is the third edition of our ‘Monthly Economic Monitor’ blog series and provides more details about this data and its implications. This month, we focus on new data about South Tyneside’s businesses and their survival rates. Within this blog, the terms ‘business’ and ‘enterprise’ have been used interchangeably – for further information see the references section at the foot of this post.

How many businesses are there in South Tyneside?

As of 2024, there were 3,230 businesses in South Tyneside. Most businesses in South Tyneside are ‘micro’ (88.2%) which means they have less than 10 employees. 9.6% of the borough’s businesses are small (10-49 employees), 1.5% are medium (50-249 employees) and 0.5% are large (250+ employees). More than 95% of UK businesses are small to medium-sized enterprises (SMEs) with fewer than 250 employees. They account for around 45% of total revenues and around 60% of private sector employment.

| Figure 1 – Top three industries by enterprise | ||

| Area | Top Three Industries | % as a proportion |

| South Tyneside | ‘Construction’ | 14.9 |

| ‘Professional, scientific & technical’ | 13.9 | |

| ‘Retail’ and ‘Accommodation & food services’ | 10.4 | |

| North East | ‘Construction’ | 14.3 |

| ‘Professional, scientific & technical’ | 14.1 | |

| ‘Accommodation & food services’ | 9.2 | |

| England | ‘Professional, scientific & technical’ | 15.8 |

| ‘Construction’ | 14.0 | |

| ‘Business administration & support services’ | 8.6 | |

Note: In South Tyneside, there were 335 enterprises in both ‘Retail’ and ‘Accommodation & food services’ broad industry groups.

As shown in Figure 1, South Tyneside has a higher proportion of businesses within the ‘construction’, ‘retail’ and ‘accommodation & food services’ industries than the North East and England and a lower proportion of ‘professional, scientific & technical’ businesses. This data comes from a snapshot of the Inter Departmental Business Register (IDBR) collated by the Office for National Statistics (ONS) using Value-Added Tax (VAT) trader and Pay As You Earn (PAYE) employer information. The IDBR is used to determine business counts, size, activity, deaths, starts, reactivations, and industry type.1

Within UK Business data, businesses are registered as active if they have employment or turnover figures in the month of March of a given reference year. In some cases, businesses often do not have employment or turnover figures but do have a role within an enterprise group (such as a parent company). The ONS excludes these cases from their business surveys and quarterly/annual business demography publications.

Active Enterprises and Business Survival

Business demography data is released annually. The most recent release was in November 2024 and covers the period of 2018-2023. It is calculated using figures from the IDBR.2 While we have included the latest available data (2024) on the number of businesses above, the OECD manual on business demography statistics recommends waiting two years after the reference period to allow for ‘reactivations’. This is where a dissolved or revoked business returns to ‘active’ status. This means that there is a delay in calculating business births, deaths, and survival rates.3

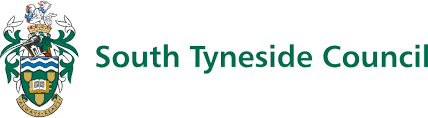

In 2023, South Tyneside had 3,730 active enterprises. In this dataset, active enterprises are defined as businesses that had either turnover or employment at any point within the reference year. This was a five-year low, just over 300 less than the 2019 peak of 4,035 but only 70 less than in 2018.

435 enterprises (92.6%) survived one year, 330 (70.2%) survived two years, 245 (52.1%) survived three years, 200 (42.6%) survived two years and 170 (36.2%) survived five years.

South Tyneside has lower business survival rates than the North East and England across all years shown. The greatest difference between local and regional / national survival rates was seen in year four, and the smallest in year one. The North East’s two, four, and five-year survival rates were marginally higher than England’s figures.

Figure 3 – Survival rates of businesses born in 2018

Proportionally, in 2023, the North East saw the joint second highest percentage of its active businesses die (alongside the North West) at 11.7%.

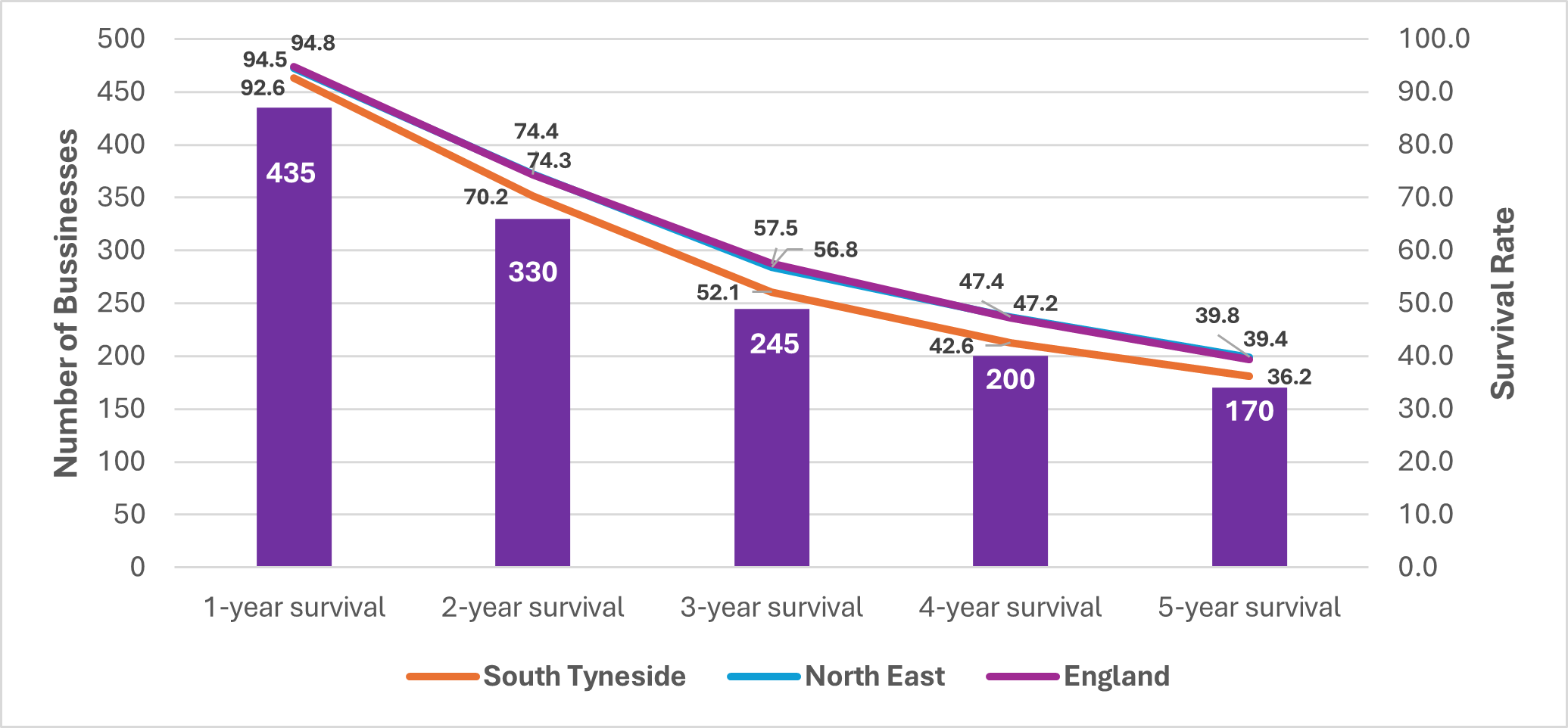

Business deaths by industry are not provided at the local authority level. However, we can look at year-on-year active business counts by industry to give us an understanding of changes over the last five years (as shown in Figure 4 below).

Figure 4 – South Tyneside businesses by broad industry group (SIC 2007)

Since 2020, unforeseen global impacts such as the Covid-19 pandemic (and related supply chain issues), rising inflation, interest rates, energy cost pressures and economic inactivity due to long-term health conditions have posed challenges for businesses nationwide. Local and regional intelligence received from businesses and public sector colleagues has attributed one or more of these factors to challenging operating and/or trading conditions at some point over the last five years.

In December 2020, the ONS published a summary report on the impacts of the pandemic on different industries throughout the UK. The data covers January 2019 – October 2020. For context, the first lockdown measures were announced on 23rd March 2020. All non-essential businesses were forced to close or otherwise pause operations whilst all non-essential workers and all other residents were legally required to stay at home to limit the virus’ spread. The report showed that the accommodation sub-industry4 suffered major blows to total turnover at the introduction of lockdown measures, with hotels taking the biggest hit, whilst services such as hospitality – including pubs, restaurants, and hotels – recorded almost no output in April and May.

High-street retailers were also significantly impacted – in February 2020 (the month prior to lockdown), internet sales as a proportion of total retail sales were less than a fifth (19.1%), though by May that same year almost a third (32.8%) of all retail sales were done online. Internet sales dropped gradually from 2021, however, as shown in the ONS’ internet sales chart, online sales have not returned to their pre-pandemic levels.

Larger or chain retailers (such as department stores) who sold ‘essential items’ (e.g. food and medicine) or had food halls and cafes were able to remain open. According to the ONS, these businesses saw less of an impact to sales across the pandemic compared to those who had to weather the transition period to mostly online sales. Similarly, food stores saw increases to sales during the pandemic afforded to panic buying at the onset of lockdown, before falling below pre-pandemic levels by July to August 2020.

The Bank of England published a report in November 2020 noting that because of lockdown and less household spending, there was an increase in household savings particularly among wealthier households. The BoE’s survey, conducted in the run up to this publication, found that only 10% of households who increased their savings during the pandemic intended to spend the money they had saved, whilst 70% said they planned to hold them in their bank accounts.

Analysis from the ONS found a similar spike in savings, particularly in Q2 of 2020. The analysis states that the purpose of saving is usually to increase future resources available for spending and protect against unexpected changes in income. The pandemic introduced another reason – saving forced through the inability to spend following government restrictions on physical movement and social interaction. Considering the findings of these two analyses, we see a clear indication of money being diverted from the UK economy and instead into personal or household savings (where disposable income allowed).

Figure 5 – South Tyneside micro enterprises

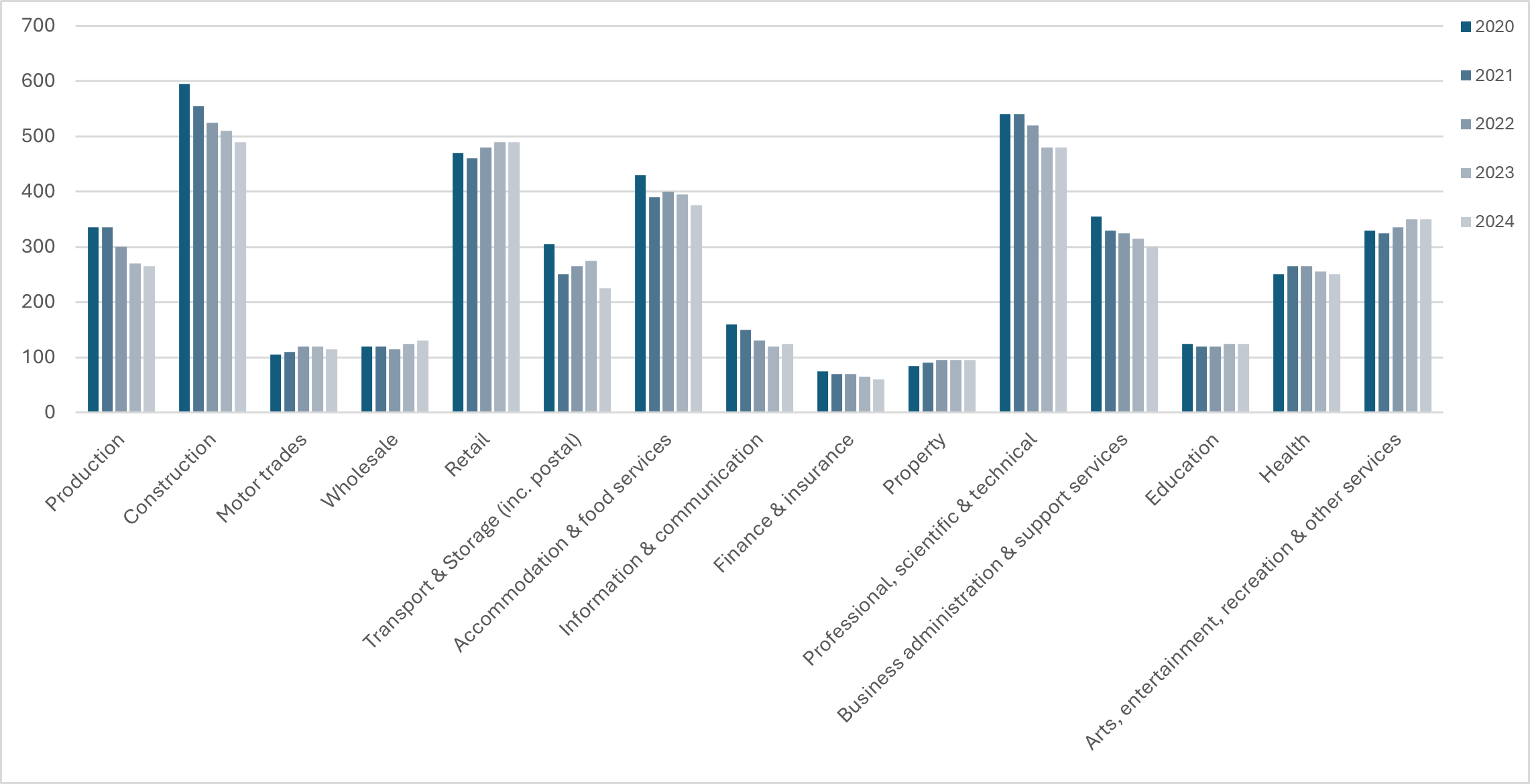

Figure 6 – South Tyneside small enterprises

Figure 7 – South Tyneside medium and large enterprises

There was a marked decline in active SMEs post-2020 (see Figure 5, 6, 7). Interestingly, the number of active small and micro enterprises in South Tyneside increased by 360 (8.8%) and 20 (6.7%) in 2020, respectively. The latter may be partially attributable to an increase in self-employment at the onset of the pandemic, which rose 0.7 percentage points (500 people) to 5.6% during the period of January 2020 – December 2020. This peaked at 7.8% (7,300 people) in October 2020 – September 2021, the highest recorded rate seen within the borough.5

With regard to self-employment data – the confidence intervals (which give an indication of how accurate estimates are) for these measures are somewhat broad, therefore we can’t be sure there was a significant change in self employment rates.6

The number of large enterprises in South Tyneside was mostly unchanged since 2018, unlike SMEs. Analysis published in October 2020 by the Bank of England found that smaller enterprises are more likely to operate in sectors more vulnerable to the impacts of the pandemic. According to the BoE, these sectors include accommodation and food, arts and recreation, construction, retail and wholesale, manufacturing, utilities, and information and communication. Referring to Figure 4, these are some of the most prominent industries within South Tyneside.

The BoE’s analysis also stated that smaller enterprises typically have less external financing options open to them compared to larger firms, despite an increased number of Government support loans and grants available to SMEs during and following the pandemic. Larger enterprises typically have a larger amount of existing capital (cash, equity, etc.) which enables them to borrow or raise larger sums of money. This means that the large proportion of both small and micro enterprises in South Tyneside – as well as those more vulnerable industries – may provide further insight into the generally lower business survival rates seen locally from 2018 – 2023.

What support is available for businesses in South Tyneside?

South Tyneside Council’s Economic Growth and Skills Team hold responsibility for attracting and supporting inward investment within the borough, alongside business support provision.

Over the last year, they have helped Curtis Instruments UK Engineering Centre and Hitachi Construction Machinery in taking up units at Monkton Business Park – creating a range of new jobs – and Woocheen as they completed their acquisition of DME Systems with scope to broaden its global manufacturing base. The Team also provided support for Pennguin on their new lease of the Viking Industrial Estate – expected to create up to 20 new jobs locally. Additionally, South Tyneside Building Supplies are in talks with the Business Investment Team (which sits within the Economic Growth and Skills Team) with aims to develop the newly acquired McNulty Car Park into industrial units.

They also support our four managed workspace facilities in Jarrow, Boldon and South Shields which provide an environment for our small businesses to expand and aim for success. Notable examples of businesses growing into larger premises within the borough include HTG and DME Systems, both having created key employment opportunities, accessed by our residents, which continued business success. Occupancy levels at these business centres have remained at a healthy 90% and currently house around 180 businesses employing over eight hundred staff.

The Business Investment Team offers a range of support, including (but not limited to):

- Planning, property search and business rate assistance in collaboration with local property agencies

- Practical day-to-day operational support, including around recruitment and training

- Business case development, including sector research and intelligence

- Finance sourcing and access

Additionally, South Tyneside Works, the local employment and skills provider operated by South Tyneside Council, closely collaborates with local employers on the rollout of skills programmes and training opportunities seeking to upskill and support residents into work. They work to ensure that the local skills base matches the requirements of local businesses, seeing that new, qualified, and highly skilled roles generated in South Tyneside stay in South Tyneside.

This is aligned with the ambitions of the South Tyneside Pledge – a local initiative in which it’s 364 members (either headquartered or operating within South Tyneside) are committed to spending, recruiting and supporting locally. This network aims to ensure money and opportunities generated within the local economy stay local – distributed amongst other local enterprises, residents, communities and VCSE (voluntary, community and social enterprise) organisations – and that knowledge sharing and support structures guarantee benefits and support for all member organisations.

A range of business support projects have and continue to be funded via the UKSPF programme:

- Start Up South Tyneside delivered by TEDCO provides support and resources needed to support new business start ups

- Scale Up Programme delivered by RTC North supports existing businesses to unlock growth through the development of scalable business models and plans

- Business and Intellectual Property Centre (BIPC), part of the national BIPC network, provides a free source of information and advice for inventors, start-ups and existing businesses

We also have a range of sector specific organisations assisting local businesses, including North East Screen who are providing support to creative industries and the NewcastleGateshead Initiative (NGI) for tourism.

Regionally, Invest North East England, the strategic inward investment agency of NECA, recently showcased the region’s opportunities in the offshore wind sector (including those situated at the Port of Tyne) at WindEnergy Hamburg, the world’s biggest wind energy trade fair, in Hamburg, Germany,

The North East Fund, launched in 2018, also provided support to SMEs regionwide, including those within South Tyneside. As of September 2024, this fund had assisted 15 South Tyneside based companies to raise a total of £14.5m, allowing firms to significantly increase operational capabilities, procure necessary equipment and vehicles, and step-up recruitment. It also provided non-financial support relating to business plan preparation to over ninety local businesses.

The North East Combined Authority (NECA) also recently launched the new North East Investment Fund. This £350 million investment aims to support 470 businesses and the creation of up to 2,300 jobs region wide over the next fifteen years. This includes the £70 million allocation of new money to directly support innovative new businesses as well as smaller enterprises.

References

[1] Within the IDBR, businesses are segregated between enterprises and local units. An enterprise (used interchangeably with ‘business’ in this blog) is an organisational unit producing goods or services and typically refers to a head office or centre of operations, whereas a local unit is an individual site (i.e. a factory or shop) within an enterprise.

[2] When comparing the UK business data with the Business Demography data, both produced by ONS, a higher number of active businesses will be reported within Business Demography. This is because the Business Demography methodology captures businesses that were active at any time during the reference year, whereas UK business is based on a snapshot of the Inter-Departmental Business Register (IDBR) at a point in time in March.

[3] The ONS estimates the number of reactivations and adjusts the data accordingly, this adjustment is applied to all industries by removing units from the death data. This can lead to different percentage adjustments at the lowest level of aggregation and, therefore, the level of reactivations is subject to some uncertainty. The latest two years in this publication are provisional and subject to revision.

[4] A ‘sub-industry’ or ‘subclass’ is applied to a registered business to further classify an enterprise within a broad industry group (UK SIC 2007). For example, a typical hotel would be listed under the ‘Hotels and similar accommodation’ sub-industry, whereas a typical restaurant would be registered under ‘Food and beverage service activities’; both of which being subclasses of the ‘Accommodation and food service activities’ broad industry group.

[5] Nomis’ economic activity data by type for South Tyneside dates back to January – December 2004.

[6] During the period of January 2020 – December 2020, confidence intervals stood at 1.8. This means that if the survey was conducted 100 times with different samples, we would expect the self-employment rate to be between 3.8% and 7.4% 95 of those times. Caution should therefore be taken when interpreting this data.